Where in 1s 8.3 VAT write-off. Accounting for "input" VAT as part of expenses: allowed cases and nuances. Supplier VAT not claimed for deduction

Many accountants are familiar with such a problem when input VAT gets into the document from quarter to quarter, despite the fact that it has already been deductible a long time ago.

Consider how to detect a "hung" VAT, and, most importantly, how to fix the error, as well as:

- the reasons for the appearance of "hanging" incoming VAT;

- generation of reports in 1C to identify "hanging" VAT;

- error correction methods.

1C provides a separate system of VAT registers, so it is often difficult for an accountant to deal with “hanging” incoming VAT on a supplier invoice from past periods. This is especially important when accounting in the program is carried out with errors.

In this article, we will go in great detail, step by step, all the way from understanding the algorithm of the program in terms of incoming VAT, finding an error, and suggesting ways to fix a "hung" VAT.

Error stuck incoming VAT

Often an accountant believes that VAT is deductible, it is enough to make a posting in 1C Dt 68.02 Kt 19 and no matter how it is done. For example, these could be:

- manual VAT entries in the document Operation entered manually ;

- manual adjustment of VAT entries in documents.

It is the movements in the VAT accumulation registers, and not in the accounting accounts, that form the entries in the purchase book and in the sales book, as well as data for the VAT declaration.

Therefore, in order to analyze the errors associated with the VAT presented by the supplier, we will follow the movements of the VAT filed register.

Accounting for input VAT presented by the supplier

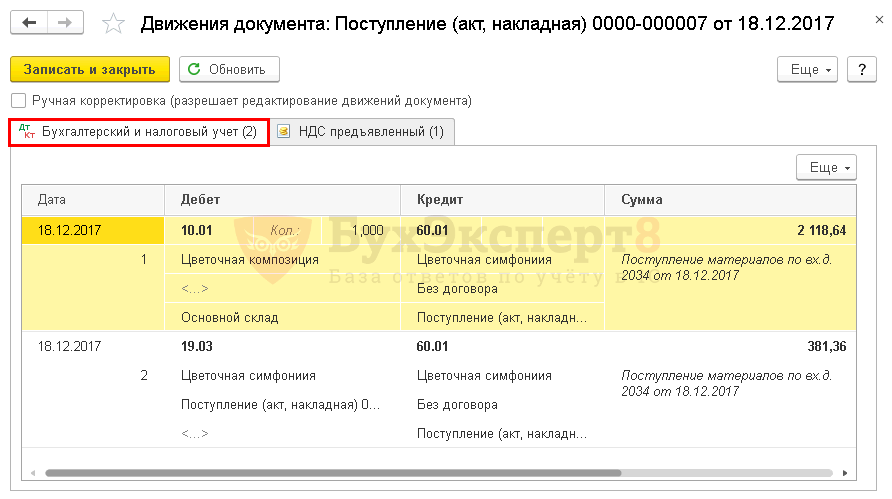

To understand the mistake made, we first pay attention to the conduct of the document Receipt (act, invoice) .

Document postings

The document generates postings:

- Dt 19.03 Kt 60.01 - acceptance for accounting of the input VAT presented by the supplier.

The document also forms a movement according to the VAT register.

- register VAT submitted – recording the type of movement Coming. This is a potential entry in the shopping book. She is waiting for the fulfillment of all conditions for the right to accept VAT deductible in the program.

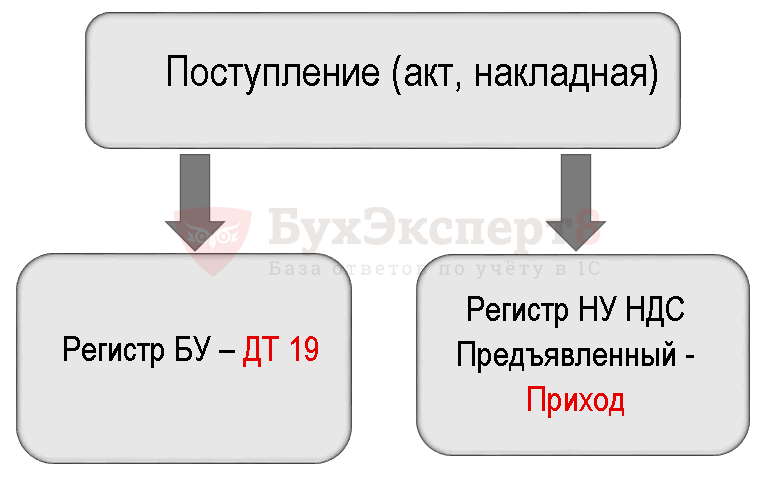

Scheme of generating VAT postings upon receipt of goods.

Write-off of VAT

As a result, VAT write-off entries were generated only for the accounting register.

Scheme of generating postings when writing off VAT manually.

In 1C, to reflect the acceptance of VAT for deduction, two parallel entries are made in VAT registers:

- Consumption by register VAT submitted ;

- register entry Book of purchases .

Document Operation entered manually does not automatically generate such entries in the registers, therefore, as a result, the input VAT "hangs" in the register VAT submitted .

Hung VAT error

When autofilling a document Formation of purchase book entries the program includes such VAT for deduction, because trying to automatically Consumption Registered VAT.

Determining the amount of hung input VAT

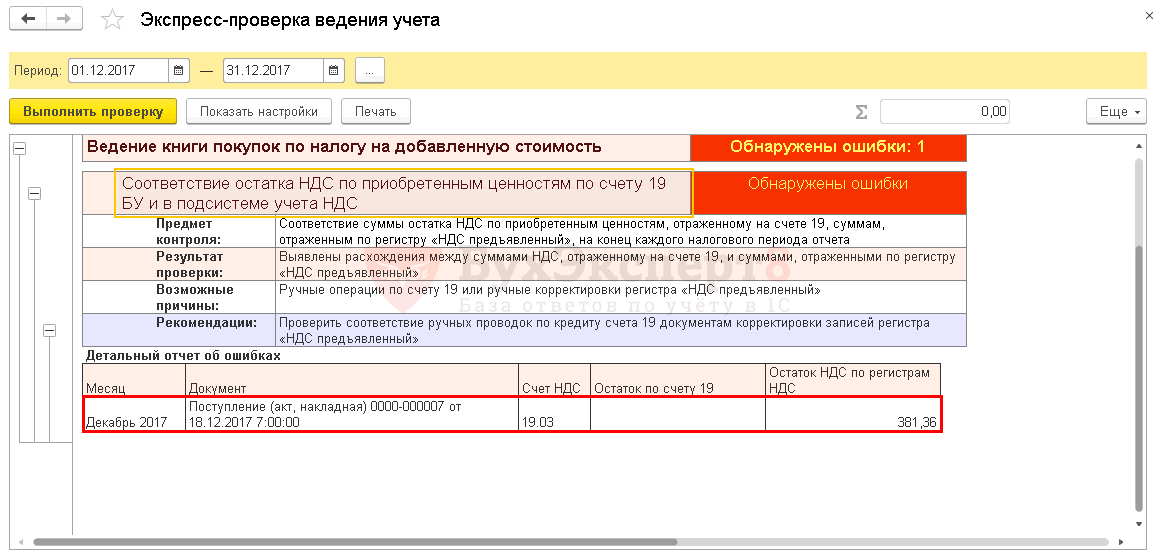

In order to correct errors related to “hung” VAT, you must first determine for which invoices and in what amounts the input VAT is “hung” in the program.

To do this, we propose to use the report Express check .

Express check

Step-by-step instructions for determining the "hanging" VAT report Express check .

Step 1: Open a report Express check : chapter Reports - Accounting Analysis - Express Check.

Step 2. Set up to search for a "hung" VAT: button Show settings - List of possible checks - Keeping a book of purchases for value added tax - check box Correspondence of the VAT balance on purchased valuables on account 19 of the BU and in the VAT accounting subsystem.

Step 3. Generate a report by button Run a check .

Other reports to identify stuck VAT

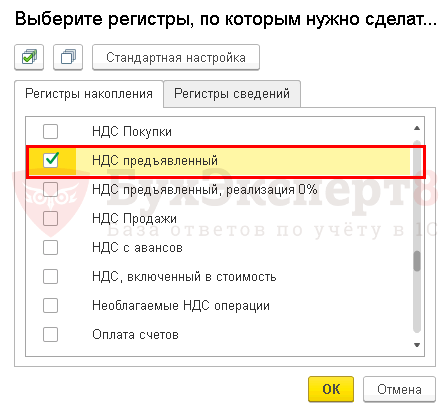

To detect "hung" VAT, you can also use the Verification of "hung" VAT setting of the Universal report. But the downside is that it does not provide a decryption in the context of invoices for which the input VAT is “hanging”.

Fixing a bug with stuck VAT

We will show how to make a correction in 1C if a “hanging” VAT is detected in the NU register.

Write off input VAT manually

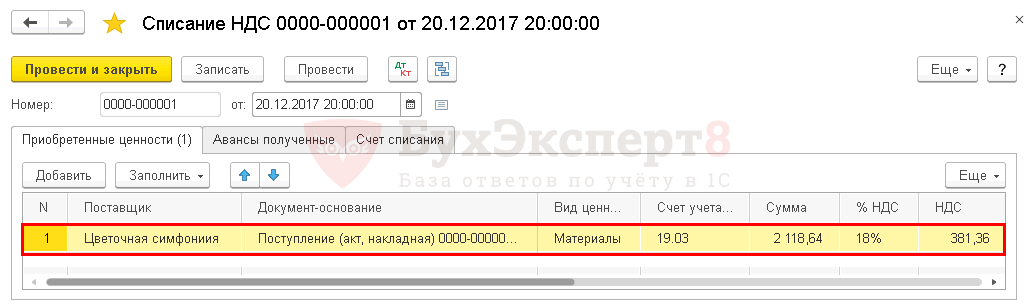

To write off input VAT according to the register VAT submitted use the document Operation entered manually .

Step 1: Create a New Document Operation entered manually : chapter Operations - Accounting - Operations entered manually - button Create - Operation.

Open the VAT register selection form by clicking the button MORE - Register selection.

Step 2. On the tab Accumulation registers check the box VAT submitted .

Step 3. Go to the tab VAT submitted and by button Add Enter your VAT information.

tab Accounting and tax accounting is not filled. The posting to write off VAT from the credit of account 19 has already been made. Entries are formed only according to the VAT register presented.

Step 4. Save the document by clicking the button Write and close .

Step 5. Check the completion of the document Formation of a purchase book entry - button Complete the document .

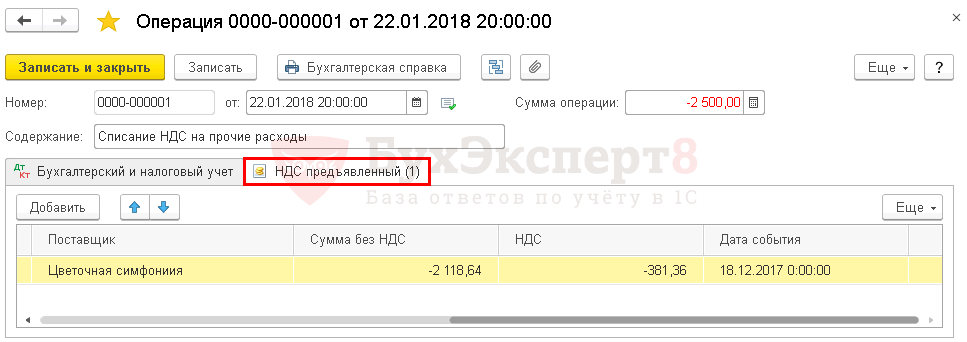

Data on the invoice of the supplier LLC "Flower Composition" is no longer included in the document Formation of purchase book entries . Correction done correctly.

Write-off of VAT by a specialized document

To write off VAT in 1C, there is a special regulatory document Write-off of VAT : chapter Operations – Period Closing – VAT Regulatory Operations – Create button – VAT write-off.

If an accountant wants to write off VAT and not deduct it at all, then it is better to use this document. He will immediately generate a transaction for writing off VAT according to the BU and write off VAT according to the register VAT submitted .

The document generates the necessary movements:

- in accounting; PDF

- in the accumulation register VAT submitted . PDF

VAT must be deducted

If, as a result of the audit, the entry for the acceptance of VAT for deduction was not previously included in the Purchase Book and was not reflected in VAT returns (Section 8), then for the possibility exercise the right to deduct VAT in document Operation entered manually you need to add and fill in a new tab on the accumulation register VAT Purchases .

Accepting VAT for deduction manually will look like this:

Register VAT submitted .

Register VAT Purchases .

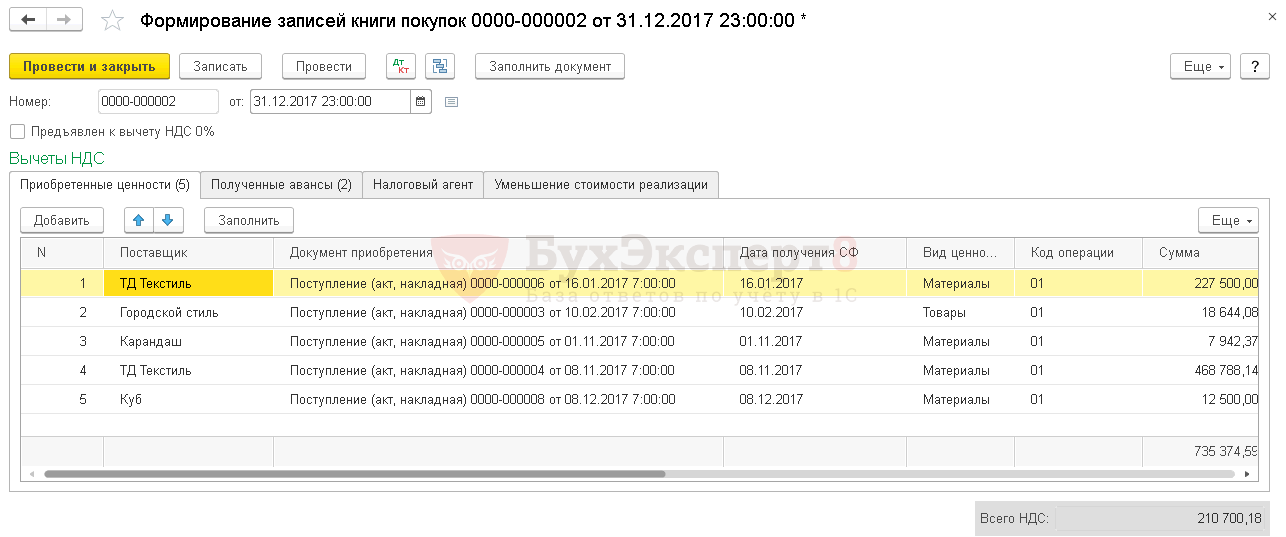

Reflection of VAT deduction in Purchase Book : chapter Reports - VAT - Purchase Book.

Writing off VAT on expenses is allowed in cases provided for in Art. 170 of the Tax Code of the Russian Federation. Often in accounting work there are situations when the amount of VAT paid cannot be deducted. You will learn about when it is possible to take into account VAT in expenses and how to correctly reflect these operations in accounting, you will learn from this article.

When is it allowed to write off VAT on expenses

In general, according to paragraph 1 of Art. 170 of the Tax Code of the Russian Federation, the amount of input VAT (the one that you pay when purchasing goods, works, services, rights or carrying out import operations) is not included in the expenses taken into account when calculating income tax (or personal income tax). However, this does not apply to the situations listed in paragraphs. 2 and 5 Art. 170 of the Tax Code of the Russian Federation. VAT can be attributed to costs if:

- the purchased goods or services are planned to be used in VAT-free transactions (confirmation of this position is in letters of the Ministry of Finance of the Russian Federation dated November 2, 2010 No. 03-07-07 / 72 and April 13, 2009 No. 03-03-06 / 1/236);

- the place of their sale is not Russia (letter of the Ministry of Finance of the Russian Federation dated 01.10.2009 No. 03-07-08 / 195);

- you, as a taxpayer, are exempt from paying VAT or are not a payer of this tax due to the application of special tax regimes (letters of the Ministry of Finance of Russia dated November 11, 2009 No. 03-07-11 / 296 and dated September 03, 2009 No. );

- the acquired goods and materials, services or rights will be used in operations not recognized by the implementation;

- assets were acquired by banks, NPFs, insurers, clearing companies, trade organizers, professional stock market participants and similar organizations (in strictly established cases).

NOTE! You can write off not only the input VAT, but also the tax calculated for payment, if you paid it at your own expense, without presenting it to the buyer.

Do simplified people need an invoice to write off VAT as expenses

From 10/01/2014, sellers are allowed not to issue invoices to simplified buyers. However, for this it is necessary to sign a special agreement that invoices will not be issued (subclause 1, clause 3, article 169 of the Tax Code of the Russian Federation). This is also evidenced by the letters of the Ministry of Finance (in particular, dated 09/05/2014 No. 03-11-06/2/44783).

In this case, such an agreement can be executed in electronic form.

If there is no such agreement, then the issue of the existence of an invoice is resolved ambiguously, and the opinions of officials are divided.

So, in the letter of the Federal Tax Service of Russia for Moscow dated June 28, 2006 No. 18-11 / 3 / [email protected] it is reported that in order to attribute VAT to expenses, an invoice is required (along with supporting documents for payment, acts, invoices). Moreover, the letter of the Ministry of Finance of the Russian Federation dated September 24, 2008 No. 03-11-04 / 2/147 states that the invoice must not only be available, but also must be filled out correctly.

However, earlier in the letter of the same department dated 04.10.2005 No. 03-11-04 / 2/94, it was stated that the document confirming the costs of paying VAT for simplified people is a payment order.

As for the courts, they believe that in this case not only invoices are suitable, but also another primary organization (an example is the decision of the Federal Antimonopoly Service of the Volga-Vyatka District dated September 19, 2005 No. A31-8435 / 19). Yes, and the tax authorities themselves, in their later letters, admitted that in order to take into account the amounts of VAT paid, payments and invoices would be enough (letter of the Federal Tax Service of Russia for Moscow dated July 19, 2011 No. 16-15 / [email protected]).

And yet, since today the law officially allows the simplified not to issue invoices, it is more expedient to draw up an agreement on the non-execution of these documents. It will take a little time, but in the future you won’t have to guess how officials and judges will once again count.

VAT on expenses charged by a foreign supplier

This situation is relevant for those who use the OSN. Regarding the accounting of foreign VAT in the expenses of Russian taxpayers, the position of the Ministry of Finance is ambiguous.

So, in a letter dated April 28, 2010 No. 03-03-06 / 1/303, officials do not allow it to be attributed to expenses, motivating their opinion by the fact that the norms set forth in sub. 1 p. 1 art. 264 of the Tax Code of the Russian Federation do not allow reducing taxable profit by the amount of taxes presented by foreign suppliers.

However, a little earlier, in a letter dated February 14, 2008 No. 03-03-06/4/8, the Ministry of Finance considered the opposite. Thus, the taxpayer, choosing one or another position regarding the write-off of foreign VAT on expenses, should understand that he may have to defend his opinion in court.

Results

From the general rule on the impossibility of including VAT in expenses, the Tax Code of the Russian Federation makes several exceptions, including the further use of the acquired in transactions not subject to VAT. In particular, VAT can be included in expenses when special regimes are applied. With a number of features in special regimes, the moment of inclusion in expenses is determined.

Write-off of VAT on 91 accounts is performed in a number of situations when, for some reason, it is illegal to accept the input tax for deduction (for example, the absence of an invoice in the presence of a separate VAT amount in TORG-12). This article covers common cases in which tax should be charged to other costs.

In accordance with the current legislation, it is lawful to accept the input tax for deduction only for travel expenses for business trips, that is, in cases where the costs incurred are directly related to the main activity of the organization.

If the business trip was non-productive in nature, then it is advisable to write off the tax to other expenses (Dt 91 Kt 19). Due to the fact that these costs are excluded when determining the taxable base for income tax, the acceptance of VAT for deduction is illegal.

In addition, there are certain nuances in the preparation of travel documents for a work trip in order to accept tax deductible. Mandatory conditions:

- The presence of an invoice from the hotel, including the required details of this document in accordance with Art. 169 of the Tax Code of the Russian Federation. In this case, the invoice must be issued for the organization, and not for the seconded employee, otherwise the acceptance for tax deduction is not feasible.

- Availability of BSO (strict reporting form), drawn up in accordance with the standards approved by the Decree of the Government of the Russian Federation of 05/06/2008 No. 359. BSO is confirmed by air and rail costs. Hotels can also provide forms of strict reporting (invoice is not needed).

IMPORTANT! In the submitted documents confirming travel expenses, the amount of VAT presented must be displayed as a separate line.

When deciding on the deduction of VAT on other documents not provided for by law, you need to remember the possibility of conflict situations with tax authorities.

Absence of an invoice for allocated tax in closing documents

A common situation with cash payments is the absence of an invoice for the allocated tax in the act or checks. In the absence of a document, the acceptance for deduction of the presented VAT is illegal. Therefore, if it is impossible to receive an invoice for these purchases, it is advisable to write off the tax to account 91 (directly or through account 19).

Expired statute of limitations for accepting tax for deduction

A 3-year period is legally established when input VAT can be deducted. There are situations when it was not possible to reflect the tax deduction for this period (for example, the absence of an invoice from suppliers). In this case, the amount of VAT presented relates to other expenses on account 91.

Also, the assignment of VAT (but not input, as in previous cases, but already accrued for payment to the budget) to account 91 upon the expiration of the limitation period is carried out when the accounts payable to the customer are written off according to the advance payment received from him. According to Russian law, upon receipt of prepayment, the supplier is obliged to issue an advance invoice. According to the issued document, the tax accrued for payment is reflected on account 76 “Advances received”. From the specified account, VAT can subsequently be presented for deduction: when selling goods or when returning funds to the counterparty. If the 3-year limitation period has passed and the debt is written off, the VAT amount is debited simultaneously with the debt to account 91 to the corresponding sub-accounts: the debt to the counterparty refers to the income of the organization, presented with the advance payment of VAT - to the expenses:

- Dt 62.2 Kt 91.1 - accounts payable to the customer are written off;

- Dt 91.2 Kt 76 “Av. floor." - VAT, previously paid to the budget from the advance received, was written off.

Transactions with special features of the transfer of ownership

The asset purchase agreement may provide for a special transfer of ownership of the property after full payment for the goods. At the same time, the supplier hands over the closing documents, including the invoice, when the assets are actually shipped.

In such a situation, difficulties arise with the acceptance of tax deductible. In fact, the property was shipped, receipt documents were provided, the goods were credited (accounting is kept on off-balance accounts until the transfer of ownership). On the other hand, the goods have not yet passed into the property of the organization, and therefore questions may arise from the regulatory authorities. Based on this, it is more expedient to leave VAT “hanging” on the debit of account 19, and after transferring the payment, accept it for deduction. If suddenly the organization did not have time to pay its supplier, and the latter was liquidated, then it will need to attribute VAT from account 19 to other expenses: Dt 91 Kt 19.

***

So, in some cases (for example, when there is no invoice in the presence of a separate VAT amount in TORG-12), input VAT cannot be deducted from the budget, so it is advisable to attribute it to account 91 in order to avoid conflict situations with controllers.

The video was made in the program "1C: Accounting 8" release 3.0.41.39.

For a recommendation article explaining in detail whether VAT can be deducted if the goods are purchased by an employee for cash, see the "Value Added Tax" reference book in the "Taxes and Contributions" section in IS 1C: ITS.

The procedure for writing off in "1C: Accounting 8" (rev. 3.0) VAT, not confirmed by the supplier's invoice, depends on how the receipt of goods and materials is registered in the program.

If the receipt of goods and materials is registered using the Expense report document, then on the Goods tab, when filling out the tabular section, the allocated VAT amount must be indicated in the VAT field. Since no invoice has been received from the vendor, the SF flag should be disabled. When posting the Advance report document, the VAT amount will be automatically written off to the debit of account 91.02 under the item Write-off of allocated VAT for other expenses (this item is a predefined element of the Other income and expenses directory). In the form of the Write-off allocated VAT for other expenses, the Accepted for tax accounting flag is disabled, so the debit of account 91.02 reflects a constant difference in the amount of VAT.

If goods and materials received are credited using the Receipt document (certificate, invoice), then when filling in the table of goods, the allocated VAT amount must be indicated in the VAT field. Since the invoice from the supplier has not been received, the details Invoice No. and from are not filled. When posting the Receipt (act, invoice) document, the allocated VAT amount remains on the account on March 19, and this amount must be written off in a separate operation VAT write-off (section Operations - Regulatory VAT operations). The VAT write-off document can be filled in automatically according to the receipt document(s) by clicking the Fill button. The account and analytics of VAT write-off will also be filled in automatically - 91.02 Write-off of allocated VAT for other expenses.

buh.ru

How to write off VAT in the 1s program?

The activities of each organization on the general taxation system are associated not only with the shipment of products or the provision of services, but also with the acquisition of materials, services and works from suppliers and accounting.

If counterparties - VAT payers can officially confirm the sale of their products, works or services with invoices (universal transfer documents), then the organization has the right to write off the amount of its own tax at the expense of "incoming". In other words, the legislation provides an opportunity to deduct (write off) the VAT presented by suppliers and sellers from the total amount of tax liabilities, that is, not to pay it.

On what basis is VAT deducted?

To apply the legal right to write off a certain amount of value added tax, the corresponding business transaction with the counterparty must be confirmed by an invoice, waybill, act of work performed (services rendered).

The right to a tax deduction and the corresponding accounting entries arises only when:

- All received goods are credited;

- Works are performed, services are provided and reflected in accounting;

- Delivery of all purchased materials and performance of works are accompanied by current invoices.

The right to a deduction for the incoming value added tax appears with the mandatory confirmation of a business transaction by an invoice (universal transfer document) of the counterparty, drawn up in accordance with the requirements of Art. 169 of the Tax Code of the Russian Federation.

If the invoice is incorrect or missing, then the tax received cannot be deducted. In this situation, the tax is included in other expenses and cannot be taken into account in tax accounting. If the company is not a payer of value added tax, then its amount increases the cost of goods sold.

In what cases is the document "VAT write-off" used?

In the program 1C: Accounting 8 (rev. 3.0), the deductibility of the tax presented by the counterparty is implemented using the document "VAT write-off", which involves manually attributing the received tax to costs. It is entered on the basis of "Receipts of goods and services" and is filled in automatically according to the data of the "VAT submitted" register, containing subconto 19 of the account.

Write-off of value added tax may be required, for example, when purchasing goods and other valuables by an accountable person. The sales receipt indicates the amount of tax, but the invoice is not provided.

When preparing an advance report on the posting of goods, works or services, the incoming value added tax is by default assigned to other costs without reducing the income tax base.

Sometimes, instead of being deductible or included in the cost, the received value added tax must be charged to certain accounts. For example, such a need arises when:

- VAT should be debited to 91 accounts instead of the account for posting valuables, works or services, and therefore it cannot be included in the cost, for example, when there is no seller's invoice;

- The organization charges employees the cost of a number of services for the amount used in excess of the limit. In this case, VAT in the given proportions is charged to account 73;

- When rationing advertising costs, VAT must be deductible when recognizing costs for tax purposes. In this situation, the residual amount of tax at the end of the year is written off to 91 accounts;

- It is necessary to correct the balances on account 19 due to errors in previous periods.

Such operations are reflected in the document "VAT write-off". In the program 1C: Accounting 8 (rev. 3.0), it is now possible to enter its data on receipts, which greatly simplifies this process and allows you to accurately fill in all the necessary details.

How to properly issue a "VAT write-off" in the 1C program

You can create a document in 1C in the following ways:

- Input based on receipts, in particular, "Receipts of goods and services";

- Using the bookmark "Accounting, taxes, reporting", selecting the journal of regulatory VAT operations in the corresponding menu and creating a new document.

Let's analyze the order and nuances of registration of this document, starting with the form (photo No. 1).

Photo No. 1. The form for creating "VAT write-offs"

Photo No. 1. The form for creating "VAT write-offs"

The tab "VAT to be written off" is filled in according to the data corresponding to the analytical sections 19 of the account according to the register "VAT submitted". The name of the underlying document, the name of the supplier, the amount and the invoice are already entered in the appropriate fields.

Additionally, the user enters:

- Amount without tax;

- Type of values;

- Tax percentage;

- Date of

blog.it-terminal.ru

Writing off VAT on expenses - accounts payable, in tax accounting, postings, in 1C

Amounts received from suppliers may be included in the cost of goods or other expenses in accounting.

General information:

The inclusion of incoming VAT in expenses for a certain category of taxpayers is a prerequisite for accounting.

Organizations and individual entrepreneurs using special taxation regimes cannot deduct or refund tax due to the lack of a VAT tax base.

As part of VAT expenses, enterprises take into account:

- Applying USN.

- Having UTII.

- located on PSN.

- Using DOS, but receiving tax exemption.

When determining the conditions for accounting for VAT, export operations are excluded as part of the costs. The application of VAT taxation at the rate of "0" does not oblige organizations to include tax in costs.

Enterprises in a number of cases write off VAT on expenses (for activities with the main taxation system), if the goods or products are not used in income tax accounting.

An example is the case of an organization that provides warranty service along with repair services. The cost of spare parts installed under warranty is compensated by the manufacturer.

Parts are written off at the time of installation in full, including VAT.

Normative base

Accounting for VAT when writing off as an expense is determined by the Tax Code of the Russian Federation. Accounting for the VAT write-off procedure is carried out in accordance with Art. 170 of the Tax Code of the Russian Federation.

For the accounting procedure, it is necessary to use the Methodological Guidelines for Accounting for Inventories.

About order

The write-off of the tax on expenses is made only on the basis of documentary evidence. It is necessary to distinguish between accounting for an organization with a complete absence of transactions subject to VAT.

If an organization applies a special regime:

- the amounts of VAT charged by suppliers are taken into account in the cost of goods at the time they are put on warehouse records;

- the amount of tax on the purchase of fixed assets or intangible assets is included in the initial cost of the object.

It is somewhat more difficult to write off the tax as part of the costs when the organization maintains several regimes. If there are regimes with VAT and non-taxable regimes, it is necessary to keep separate records.

The division of income and expenses by type of activity is a prerequisite for including tax in expenses.

According to Art. 170 of the Tax Code of the Russian Federation, it is necessary to ensure the maintenance of separate accounting for obtaining VAT amounts applied for deduction or related to expenses.

The organization independently determines the procedure and term for dividing the received and sold assets - immediately upon receipt to the warehouse or as they are shipped to production.

VAT on general business expenses is determined at the end of the period - month, quarter. The division is made on the basis of the proportion of the shipment or the proceeds received from transactions subject to VAT and not subject to VAT.

In the case of a clear definition of expenses by type of activity, it is not required to make calculations depending on revenue.

Options for a clear allocation of costs and, accordingly, VAT, can be leased premises, transport, fixed assets, including movable property and other types of expenses assigned to the type of activity.

Where to write off

The VAT received as part of the documented amounts of the value of assets can be written off as part of the cost or among other expenses.

The taxpayer can dispose of the received VAT:

- By determining the amount as part of the expenses, if the received assets are used to conduct activities that are not subject to VAT.

- Do not immediately take into account the tax in expenses upon receipt of documentary confirmation of supplies if it is possible to use goods, products in generating income with separate accounting for the enterprise.

The cost of goods and products received is included in the cost price. The amount of VAT received is included in the asset received.

Depending on the accepted accounting policy, transportation costs for the delivery of goods may be included in the cost of goods.

Other expenses that may include VAT when conducting non-taxable activities may include utility bills, communication services, stationery costs and other types of expenses of the enterprise.

Write-off is not made

In the process of doing business, there are cases with the transition of the enterprise to another type of taxation. In the event of a transition from the general regime, it is necessary to take an inventory of the inventory balances in the warehouse.

Before the transition, enterprises try to reduce the balance of goods in the warehouse:

- VAT previously accepted for deduction on goods received must be restored and paid to the budget (Article 145 of the Tax Code of the Russian Federation);

- Goods that will be used in activities not subject to VAT will be accounted for at the cost of posting - excluding VAT amounts as part of the cost price.

The taxpayer cannot increase the cost of posting by the amount of VAT received before the transition. Other expenses do not include VAT.

No further deduction of the recovered amount will be made in the event of a change in the taxpayer's circumstances. Accounting for fixed assets and intangible assets is carried out in a similar manner.

If there is separate accounting when adding activities that are not subject to VAT, the taxpayer shall restore VAT on a quarterly basis.

How to write off VAT on expenses

The write-off of VAT on expenses is made at different points in time, determined by the presence of compatible regimes and the inclusion of tax either in the cost price or in other expenses.

Step-by-step instruction

When writing off tax to cost:

- It is necessary to obtain documentary evidence of the value of the asset and the accrued VAT.

- For taxpayers applying UTII, the amount of VAT is included in the cost of goods or products upon posting.

- Taxpayers applying the simplified tax system "income" can consider the tax as an expense at any time, the order of inclusion does not affect taxation.

- The amount of input VAT under the simplified tax system "income minus expenses" is taken into account only after payment to the supplier on the invoice.

- With separate accounting, the write-off procedure is governed by accounting policy.

When writing off VAT as part of other expenses:

Reflection in accounting and tax accounting (postings)

Postings are created in accounting:

Similarly, postings are made with expenses attributed to other expenses. In this case, there are no differences between tax accounting and accounting.

How is a write-off in 1C

Keeping records using the accompanying 1C program simplifies the write-off of VAT due to process automation:

- In the accounting policy tab regarding VAT accounting, you must select “include in the cost or write off as expenses in accordance with Art. 170 of the Tax Code of the Russian Federation.

- The document that will produce the movement is the “requirement-invoice”.

- In the "stocks" tab, you must select batch accounting or by quantity and amount.

If you need to write off VAT on expenses before moving goods and materials, you can apply a manual posting that does not affect inventory.

How to write off with USN

A feature of VAT accounting under the simplified tax system is the recognition of tax as an independent expense.

The amount is placed as a separate line in the book of income and expenses with subsequent reflection in the single tax declaration.

When accounting, it is necessary to take into account the cash method of maintaining income and expenses.

Writing off VAT to expenses has a number of features:

- it is possible to direct the amount of tax on goods to costs only after the actual sale of the asset. On this occasion, there is a clear position of the Ministry of Finance, expressed in a letter dated September 24, 2012 No. 03-11-06/2/128;

- the basis for writing off the VAT of materials is their transfer to production.

- when purchasing fixed assets or intangible assets, on which VAT has been charged by the supplier, the write-off is not made in a separate line, the amount is included in the property. When using the USNO regime “income minus expenses” (clause 2 of article 346.18 of the Tax Code of the Russian Federation), depreciation of the asset is charged. Subsequent inclusion in the composition of costs in equal parts allows you to write off VAT during the entire period of operation.

All expenses, including indirect tax, must be documented and economically justified.

The structure of documents includes contracts, waybills, acts, invoices, waybills, bills of lading and waybill. To include VAT in the costs, the supplier must comply with the rules for issuing invoices.

Write-off of accounts payable with VAT

The amounts of overdue accounts payable are subject to write-off after the expiration of the generally established limitation period - 3 years.

Organizations include amounts in non-operating income. The procedure is regulated by Article 250 of the Tax Code of the Russian Federation.

Accounts payable may include outstanding obligations to suppliers, amounts of commodity credits for deferred deliveries, as well as VAT accrued according to documents.

The legislation determines whether the write-off of accounts payable with an expired limitation period is subject to VAT.

In the case of writing off the cost of goods in advance delivery, the provision of work, the taxpayer should not recover the VAT indicated in the form of a deduction. The tax authority's position is based on the fact that the goods have been received.

In favor of confirming the payment of tax to the budget is the fact that the taxpayer must pay VAT upon shipment, regardless of the payment received.

Separately, it is necessary to consider the issue of accounting for VAT on advances received. On this issue, a letter of the Ministry of Finance of the Russian Federation dated 07.12.2012 No. for No. 03-03-03/1/635.

The taxpayer has an obligation to pay tax on advances received on account of future deliveries.

When writing off amounts of overdue debt from advances, the amount of VAT previously paid to the budget cannot be claimed for deduction.

According to the letter of the Ministry of Finance of the Russian Federation No. under No. 03-03-03/1/58, VAT amounts when writing off debts are not included in expenses or income.

The VAT invoiced by the supplier of goods, works, services is paid by the enterprise when making settlements for deliveries.

In the absence of grounds for applying the deduction, the amount of tax may be included in the expenses of the organization or individual entrepreneur.

The operation must be carried out in accordance with documentary evidence.

Write-offs to expenses must be made within a period of business that is clearly defined by law, taking into account the cash basis or separate accounting of the enterprise.

buhonline24.ru

Articles and publications

Sometimes it is required that the VAT presented by the supplier not be deducted or included in the cost, but written off to some other account. Examples include the following situations:

- VAT must be written off to account 91.02, and not to the account for assigning valuables, and therefore inclusion in the cost cannot be used, for example, if there is no supplier invoice;

- the organization re-bills for paying for mobile communications to employees (in excess of the limit), then VAT must also be charged in some proportion to account 73.03;

- when rationing advertising expenses, VAT should be deductible as expenses are recognized in tax accounting for income tax, in this case, the balance of VAT at the end of the year should be written off to account 91.02;

- an error occurred in the previous period, and it is necessary to correct the balances on account 19.

Such operations should be reflected not in an accounting statement, but in a special document “VAT write-off”. In the latest versions of Enterprise Accounting 3.0, it became possible to fill out a document based on the “Receipt of goods and services”, which greatly simplifies the filling procedure and avoids data entry errors. Consider the form of the document and the features of its filling.

On the "VAT to write off" tab, the fields corresponding to the "VAT submitted" register (a special register that expands the analytics of account 19 in the program) are indicated. These fields also correspond to account 19 analytics: Vendor, Base document, VAT account, and VAT amount.

The following fields must be additionally filled in the register: Type of value, amount without VAT, VAT rate and date of payment. These additional fields must be filled in especially carefully, because. if filled in incorrectly, incorrect balances will be obtained in the “VAT submitted” register.

If the filling is done manually, then you should get the balances according to the “VAT submitted” register and fill out the tabular part of the document on them. The balances in the register "VAT submitted" can be viewed in the report "Universal report". It is necessary to select the register "VAT submitted" and in the settings add the Indicators corresponding to the columns of the tabular part of the document.

On the “Write-off account” tab, the account and analytics of the VAT write-off are indicated. You can choose any account. When filling out on the basis of the document "Receipt of goods and services", account 91.02 and the item of other income and expenses "Write-off of allocated VAT for other expenses" are automatically set.

When posting, the document generates postings of the type DT “Debit Account” - KT 19 and movements according to the register “VAT submitted”. The correctness of filling out the posted document can be checked with the “Universal Report” report; you need to fill it out in the same way as before. When checking, you should pay attention to the fact that the lines with negative income correspond in terms of analytics to lines with balances.

If after reading the article you still have questions, you can ask them in this form. We will try to answer any questions about reflection in programs on the 1C: Enterprise 8 platform on the next business day.

Any accountant knows that the presented VAT under certain conditions can be accepted for deduction. However, there are cases when, due to legislation or the current situation, this is not possible.

When is it allowed to account for VAT paid as part of expenses that reduce the income tax base?

What does the Tax Code say about this?

How do the tax authorities interpret its norms, and is their point of view always supported by judicial practice?

All this will be discussed in this article.

The current legislation provides for well-defined operations, when the VAT presented to the taxpayer can be included in the cost of goods, reducing the base for calculating income tax. This is stated in the article 170 tax code. According to paragraph 2 of this article, it is possible to attribute tax to the costs of production and sale of goods (works, services) in the following cases:

- if they are used to carry out VAT-free transactions - Article 149 of the Tax Code;

- if the products manufactured with their use will be sold outside the territory of Russia - Article 148 of the Tax Code;

- if the person acquiring them is not a VAT payer or is exempt from paying this tax;

- if they are purchased for those operations that are not subject to VAT (for example, gratuitous transfer of structures to state bodies and other operations listed in paragraph) - 2 Article 146 of the Tax Code of the Russian Federation.

This is an exhaustive list of transactions for which input VAT can be attributed to the cost of goods, works or services, thereby reducing the income tax base.

It is worth noting that not only tax amounts presented directly upon purchase, but also restored in accordance with paragraph 3 of Article 170 of the Tax Code of the Russian Federation, can be attributed to expenses.

In other words, if the goods are used to carry out the above operations, then the VAT previously deducted on them should be restored and taken into account as part of other expenses in accordance with Article 264 of the Tax Code of the Russian Federation.

Does the taxpayer have a choice?

It is important to keep in mind that the norms of the law on tax deductions and the procedure for their application (Articles 171 and 172 Tax Code of the Russian Federation) are worn imperative character, i.e. mandatory. This means that a buyer who has been presented with VAT by a supplier does not have the right to choose whether to include the amount of tax in expenses or declare it deductible.

Thus, if the taxpayer had grounds for deducting VAT, but for some reason he did not use it, then he is not entitled to include the amount of tax in expenses.

Unrealized right to deduct VAT: special cases

A situation where a company has not exercised its right to deduct VAT may arise for various reasons. The most common of them are the following:

- lack of invoices issued by the seller;

- missing the deadline for claiming the deduction.

The first situation often arises when making a purchase in a retail network. Most often, these are some “little things”, for example, stationery for the needs of the office or refueling a car. In this case, it is unlikely to receive an invoice from the seller, and, according to the tax service, it is illegal to claim a VAT deduction based on a cash receipt. The absence of an invoice will be detected immediately when.

It turns out that it is impossible to deduct the amount of VAT on acquired valuables, but at the same time, as mentioned above, it cannot be attributed to expenses that reduce the income tax base. However, those companies and entrepreneurs who have a desire to fight for the deduction of the amount of tax in this situation in court have every reason to do so.

The decision of the Presidium of the Supreme Arbitration Court No. 17718/07 dated 05/13/2008 determined that under such circumstances it is unlawful to refuse a taxpayer to deduct VAT. This is true provided that there is a cash receipt confirming the purchase, and that the fact that the taxpayer used the purchased goods outside the taxable activity is not proven.

Nonetheless official position of the Federal Tax Service has not changed: VAT can be deducted only on invoice, and the issues of submitting other primary documents as a justification for the deduction are resolved judicially.

Speaking of the second obvious reason why a taxpayer may lose the right to deduct VAT, let us turn to clause 1.1 of Article 172 of the Tax Code of the Russian Federation. Since its entry into force, namely from the beginning of 2015, the procedure applications for VAT deduction within three years from the moment the goods are registered. However, this deadline may also be missed, for example, by mistake or due to lengthy preparation of documents. Be that as it may, it is unlawful to claim a VAT deduction outside this period. That is, in this case, the tax will have to be paid, but it will not be possible to attribute its amount to the income tax expense account.

As an illustration, let's take the situation of a Russian exporting company that took too long to collect a package of documents to confirm the zero VAT rate. As a result, she declared an "input" tax on transactions taxed at a rate of 0% beyond the three-year period, and on this basis she was denied a deduction. The amount of tax that the company had to pay was included in income tax expenses, but the Supreme Arbitration Court did not agree with this position (determination of the Supreme Arbitration Court of the Russian Federation No. 305-KG15-1055 of 03/24/2015).

An example of a situation where VAT can be attributed to expenses

Another special case is also related to the non-confirmation of the zero VAT rate, however, it is not about the tax presented by the taxpayer, but about the cost of his services calculated “from above”. The situation is considered in the letter of the Ministry of Finance No. 03-03-06/1/42961 of 07/27/2015. The department is of the opinion that if the legality of applying a zero VAT rate cannot be confirmed, then the amount of tax calculated at a rate of 18 or 10% on the basis of subparagraph 1 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation should be included in the expenses.

Making such a conclusion, the Ministry of Finance refers to the decision of the Supreme Arbitration Court of the Russian Federation dated April 9, 2013 No. 15047/12, issued in a dispute between a major Russian air carrier and the Federal Tax Service. The company was unable to collect documents to confirm zero VAT, calculated it at a rate of 18%, paid and included this amount in expenses that reduce profits. The tax service saw this as a violation. However, the SAC did not agree with this position and explained that the dispute was about VAT calculated “from above”. In this case, it is necessary to apply the rules of tax legislation on the accounting of these amounts as expenses. The court also indicated that this VAT should be charged to expenses immediately after the expiry of the 180-day period, which is provided for the submission of documents confirming the zero rate.

VAT included in bad debts

Another case where VAT is included in expenses is if it is included in receivables that are overdue and subject to write-off. Such a situation may arise as a result of an unpaid delivery or the transfer of an advance payment against which the goods were never shipped.

After three years, the debt becomes uncollectible and is written off as expenses.

In this case, the company has the right to write off the amount of receivables together with VAT. This procedure does not contradict the official point of view of the Ministry of Finance, which is reflected in the letter No. 3-07-05 / 13622 dated 03/13/2015.

It is worth paying attention to one nuance that arises when writing off bad receivables for prepayment. If the VAT presented upon its transfer was previously accepted for deduction, then when writing off receivables, the tax must be restored. This is the position of the Ministry of Finance, but many experts consider it controversial, since paragraph 3 of Article 170 of the Tax Code of the Russian Federation does not say anything about restoring VAT in this case.

On the income tax base, not only written-off receivables, but also written-off accounts payable are reflected. It arises as a result of non-payment for shipped goods or the company's failure to deliver on account of the advance payment received, when the three-year limitation period for these operations has expired. How to deal with VAT as part of such a "creditor" when it is written off? Let's consider this issue in more detail on specific situations.

If the debt of the company was formed due to the fact that the goods received were not paid for, then the amount of the debt is charged to the income tax income account in full, that is, together with VAT. At the same time, tax amounts accepted for deduction upon receipt of goods are not subject to recovery (letter of the Ministry of Finance dated 06.21.13 No. 03-07-11 / 23503).

Another case is when accounts payable were formed due to the fact that goods were not shipped against the received advance, from which VAT was paid. After the expiration of the limitation period, the amount of debt is included in the composition of income forming the base for income tax. How to deal with previously paid VAT on this amount? Logically, it should be excluded from income. However, the Ministry of Finance adheres to the point of view that the Tax Code does not allow reflecting this VAT in expenses (letter of the Ministry of Finance dated 07.12.12 No. 03-03-06 / 1/635).

But according to many experts, there is another way out of this situation. They propose to take into account in income tax income not the full amount of the prepayment received, but the amount minus the VAT paid on it. At the same time, they refer to paragraph 2 of Article 248 of the Tax Code of the Russian Federation, which prescribes to exclude from the composition of income the amounts of taxes presented by the taxpayer to the buyer. However, if the company decides to follow this path, it is very likely that it will have to defend its case in court.

Accounting for "foreign VAT"

For companies operating with partners from neighboring countries, often there are questions about how to deal with VAT, which appears in the primary documents received from them. Here it is important to understand the following: despite the fact that this tax is also called Russian, it has nothing to do with our VAT. This is a tax of a foreign state; it is calculated and paid in accordance with the legislation of the country where the partner of the company is a resident.

Thus, the tax called VAT, which appears in the invoices of a foreign counterparty, is not deductible under any circumstances.

How should the “foreign VAT” presented to the buyer be reflected in the accounting? The fact is that it does not need to be taken into account separately. It forms the cost of purchased goods (works, services) and is included in income tax expenses.

In other words, for a Russian company it makes no difference which taxes are included in the cost of goods purchased from a foreign supplier, because the full amount of the contract will be taken into account in the costs.

On the other hand, “foreign VAT” appears in a situation where, when paying for services rendered, a foreign partner, who is a tax agent, withholds this tax from the contract amount. For example, a Russian company provided services to a foreign enterprise, the cost of which amounted to 1200 conventional units (c.u.). However, the domestic firm received 1000 c.u. The partner withheld the rest of the amount in accordance with the legislation of his country as a tax agent.

How should this transaction be reported in income? The Ministry of Finance believes that in full, including withheld foreign tax. That is, in our example, the Russian company must record the income from the operation in the amount of 1200 USD. But the amount of withheld tax in the amount of 200 USD. can be attributed to expenses taken into account for income tax purposes. (Letter of the Ministry of Finance of May 18, 2015 No. 03-07-08/28428).

True, in 21 The chapter of the Tax Code does not indicate on the basis of which document the withheld tax can be accepted as expenses. Therefore, in this matter, one should be guided by the norms of the chapter 25 , and specifically articles 313 Code. It defines the documents on the basis of which the income tax withheld by the tax agent can be offset against the tax payable by the taxpayer. Thus, if a foreign partner has withheld "its own VAT" from the company as a tax agent, a document confirming this process should be required from him. If the latter is in a foreign language, it will need to be translated into Russian.

Where to attribute VAT on re-import?

Under the customs procedure for re-import, goods are placed that the exporter, for some reason, is forced to import back into the country. In practice, customs authorities usually levy VAT on the value of such goods. The legality of this can be argued, but taxpayers usually prefer to pay the tax in order to get their own product back as soon as possible. And then the question arises: how to proceed with the amount of this tax?

We note right away that it is impossible to deduct the VAT paid upon re-import. Clause 2 of Article 171 of the Tax Code of the Russian Federation lists all cases when customs VAT can be deducted, and operations for the re-import of goods do not appear there. Based on Article 170 of the Tax Code of the Russian Federation, the amount of tax cannot be included in the cost of imported goods either. After all, most likely, they will be further implemented, that is, used in activities subject to VAT.

According to experts, it is advisable to attribute the VAT withheld on the re-import of goods to the account of other expenses that reduce taxable income, as a tax paid in accordance with the law.

And although paragraph 19 of Article 270 directly prohibits the inclusion of VAT in expenses, it refers to the tax presented by the taxpayer. When re-importing, the owner of the goods does not show the withheld VAT to anyone, therefore, the specified legal norm is not applicable to this situation. This is also confirmed by judicial practice. Thus, the customs VAT withheld upon re-import can be included in other expenses taken into account when calculating the income tax base.

Related posts:

How banks assess the creditworthiness of clients Methods for determining the creditworthiness of clients in world practice

How banks assess the creditworthiness of clients Methods for determining the creditworthiness of clients in world practice

What can be made from the keys of beer cans

What can be made from the keys of beer cans

What can you do with baby food jars

What can you do with baby food jars

Monthly allowance from maternity capital Receive a one-time maternity capital payment

Monthly allowance from maternity capital Receive a one-time maternity capital payment

Monthly allowance from maternity capital Issuance of funds from maternity capital

Monthly allowance from maternity capital Issuance of funds from maternity capital